The FOAK Stage: A Start-Up Becomes a Company

The most transformational stretch of the entire Lab-to-Market journey.

It is the commercial-grade deployment of a technology or system, in a real-world operational environment, with a paying customer, at a relevant scale that could not have been credibly claimed at TRL 7, that is THE critical destination of TRL 8 for most Deep Tech boards and leadership teams. And it is an achievement worth celebrating, to be sure.

But in truth, the technical milestone is only a part of the requirement.

The other parts involve progressing operationally, commercially, and organisationally – of demonstrating that your company can build and deliver a solution repeatedly, via production facilities or partnerships recognised by the industry, with a commercial foundation and contracts in place, and an organisation capable of innovating at scale, repeatedly, in timescales required by the value chain in which it is operating.

This is the real purpose of the FOAK (‘First-of-a-Kind’) stage – the assembly of different capabilities & functions into a high-performance form that inspires confidence across different stakeholders and that will determine the company’s future. Those that treat the stage as merely a technical target with a trophy technology or unit often fail to make the most important transition of the entire Lab-to-Market journey.

This essay examines five dimensions of the FOAK stage that companies should be thinking about.

1. Where the F.O.A.K. Stage Sits in the Journey

Before examining the stage in detail, it is worth understanding where it sits in the broader risk architecture of the Lab-to-Market journey.

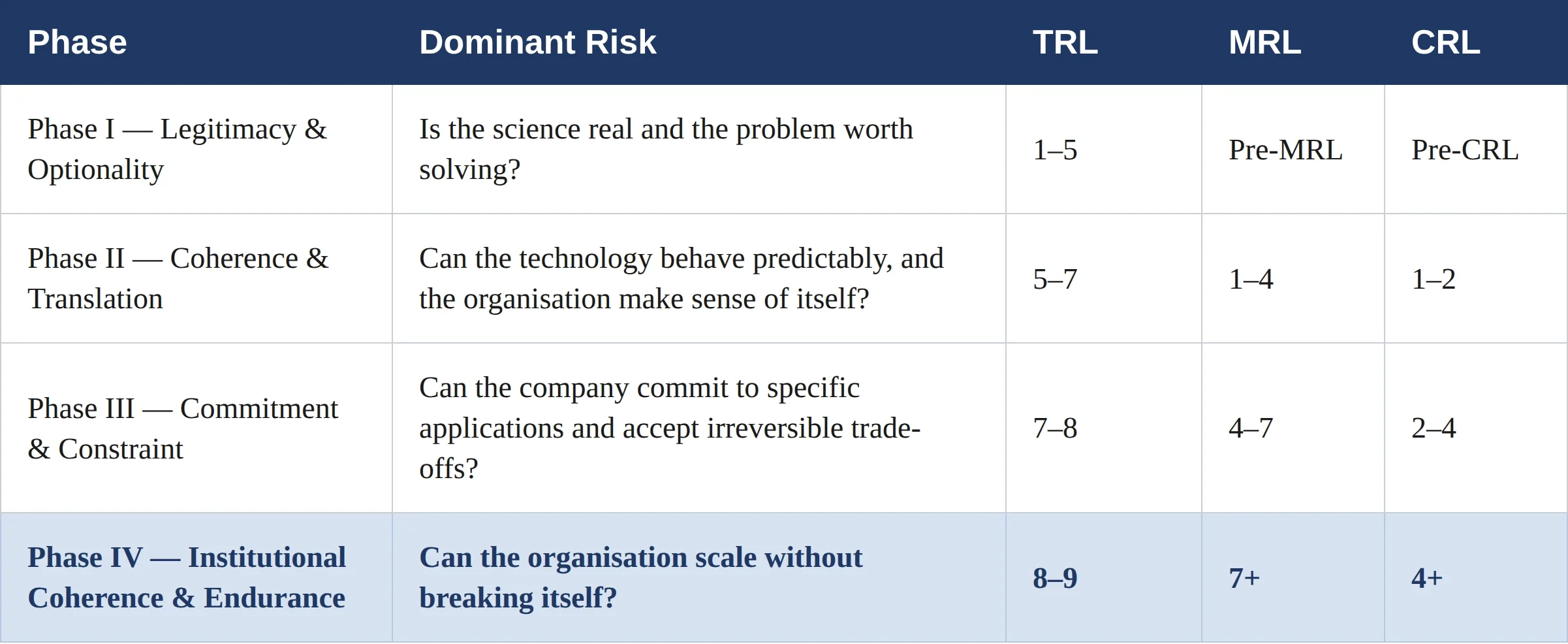

In our essay The Four Risk Phases, we describe how Deep Tech companies navigate four distinct phases, each defined by the dominant risk that, if left unresolved, will end the company’s Lab-to-Market journey. The FOAK stage sits at another of the framework’s most critical transitions, the shift from Phase III to Phase IV.

Phase III is the phase of Commitment and Constraint. Its central question – can the company make irreversible choices (around questions to do with application, pricing, unit economics, production architecture, etc.) and accept the constraints that come with them? – begins to assert itself at the tail end of the Pilot Stage and dominates the first half of TRL 8. This is the phase in which optionality, which was an asset in Phase I and a reasonable position in Phase II, becomes a liability. Pursuing a commercial-grade first deployment is, by definition, an irreversible commitment. A specific application gets locked in, as do specific supply chain partners, a specific production architecture, as do very specific economics, and very specific technical and commercial trade-offs. Much of what is built during the FOAK cannot easily be undone.

The classic Phase III failure mode is an insistence in continuing to present the technology as ‘a platform’ with a broad menu of potential applications to be decided by partners/customers. What investors, customers, and partners are asking for at this stage is a demonstrated commitment to a specific application.

As the FOAK progresses and the company moves from first deployment toward repeatability and scale, the questions of Phase IV begin to assert themselves, asking can the organisation scale without breaking itself? The systems, behaviours, and leadership styles that carried the company through Phase III may not suffice for Phase IV. Founders who may have been the company’s greatest asset in the early stages of the journey can become the most significant constraints at this stage, if they have not evolved. Tasks shift from individual problem-solving & heroics, to building a high-performance organisation that is capable of innovating, delivering, and problem-solving consistently, at increasing scale, without over reliance on any single individual.

The FOAK stage, therefore, is not a single-phase exercise, but instead, multi-dimensional. Companies that navigate it well are those that understand they are both making and living with irreversible commitments, while simultaneously building the institutional foundations that the phase demands. The leadership, technical, operational, commercial, and organisational requirements of each are genuinely different.

The four Lab-to-Market risk phases mapped onto TRL, MRL, and CRL. The FOAK Stage (TRL 8) spans the completion of Phase III and the onset of Phase IV. Phase transitions are defined by shifts in dominant risk, not by reaching a specific readiness number.

2. What ‘First of a Kind’ Actually Demands

The most recognisable manifestation of true FOAK is a commercial-grade component or system that is operating in real-world circumstances, at real-scale, with real consequences.

This means that operationally, there is a unit performing within an environment hosted by, or interacting with, the engineering of a partner or customer. This means that commercially, this unit is priced at a level the value chain would recognise and accept, and that the unit economics favour not just one partner or customer, but the entire value chain. And this means that organisationally, there exists a high-performance team that understands how they got to this point and that can serve as the foundation for the team that will take them forward.

This is not to say that every critical decision will have been made at the point of initial TRL 8 deployment. Supply chains may need to be improved or scaled up. Manufacturing processes that worked in controlled environments may behave differently in a full-scale operational context and will need to be tweaked. Interfaces with customer systems, regulatory requirements, and third-party infrastructure often introduce dependencies that are difficult to fully anticipate, no matter the level of preparation.

But – and this is important – they are also representative of challenges that require a different kind of organisational readiness than anything the company has had to demonstrate before. And they are broadly the target conditions that most lab-to-market companies should be striving for when reaching for full TRL 8 readiness.

3. From One to Many: The Nth-of-a-Kind Problem

This build toward maturity is perhaps most manifested when considering the Nth-of-a-Kind problem. And if there’s one word that best summarises the challenge, it’s ‘repeatability’.

Repeatability requires that the knowledge embedded in the team that built and deployed the first unit / device / technology can be transferred into processes, into documentation, into training, into supply chain relationships, into quality standards, without losing fidelity or without the presence of specific individuals. Such lessons need to be captured systematically and fed back into the next deployment, with an impact that will be felt across all parts of the organisation.

It also appreciates that the requirements spoken of by prospective partners and customers at TRL 5/6 are likely to have moved on, which makes up for the difference between the FOAK and the NOAK (‘Nth of a Kind’), which we touch on later. Ramping up innovation (typically via a separate R&D function that is sheltered from FOAK realisation) at this stage is how the better prepared Deep Tech companies tend to respond.

Of course, none of this happens naturally. Left to their own devices, most technical teams tend to concentrate their attention on getting the first one right and treat everything else as a distraction, which is understandable when you’re simply trying to get something to work for the first time. But the companies that emerge from TRL 8 in the strongest position are those that have found a way to run both tracks simultaneously: delivering the FOAK with the full commitment it deserves, while building the organisational and process infrastructure that Phase IV will require.

4. The Organisation That Has to Be Built

What is the new organisation that needs to be built to support the offering and the value chain being served? How should it perform?

I’ve often used the image of a Formula 1 team instead of a more traditional ‘corporate’. It’s not that corporates are ineffective – the best ones are extremely so. But it’s more that the Formula 1 image better represents the energy and culture of the innovator capable of consistently performing and delivering. Pace, precision, quality, accountability, talent density, innovation – these are the features against which the most innovative companies in the world will live or die – and it is the space into which an emerging Lab-to-Market company must be willing to occupy.

It is not for the faint of heart. It generally involves an entire transformation in the way stuff gets done. Systems dominate over individual heroics. Lean, efficient, yet highly innovative practices are refined and refined again, until the organisation operates like clockwork, with each part serving its purpose and performing at the level expected. There can be no exceptions.

As such, the team that got the company to TRL 8 is unlikely to be the team that carries it through to the market. This is one of the harder truths of the FOAK stage, and one that many founding teams resist longer than they should.

To have a chance of successfully navigating this part of the journey, founder executives (assuming they’re still an active part of the company) need to actively support what can feel like a ‘transfer of power’. Their ‘brilliance’ now belongs to the know-how of the company. It is no longer ‘about them’, but about the performance and success of the organisation they serve.

This is a good example of the Phase IV imperative in its most practical form. Can a new type of team be built, without the entire organisation breaking itself?

More specifically, manufacturing and operations leadership, at a level of seniority and experience commensurate with actual industrial deployment, typically becomes necessary during TRL 8, often for the first time. So does finance leadership with experience across different capital raising instruments, including capital markets, not just the financial management competence that has served the company at seed and Series A. Commercial leadership needs to evolve from the market discovery and relationship-building orientation of the Prototype and Pilot stages into something closer to a more sophisticated business development / sales and delivery function. And across all of these, the company needs People & Talent infrastructure that simply did not need to exist when the team could fit in a single room.

Culturally, this is disruptive. The tight, high-trust, fully-committed founding culture – where everyone knew everything, decisions were made quickly, and relationships substituted for process – encounters new people who bring different working assumptions, different professional norms, and different expectations of how a company should operate.

The companies that manage it well are those that treat culture as something to be actively designed rather than passively preserved. They are explicit about what they want to carry forward from the founding phase and deliberate about what needs to change. They introduce new leadership not just for their functional expertise, but for their compatibility with the intellectual seriousness and commercial honesty that the best Deep Tech cultures are built on. And they do this with enough urgency that the capability is in place before it is needed.

5. Innovation at Pace and at Scale

Deep Tech companies that become serious industrial players do not stop innovating once the first commercial deployment is achieved. They accelerate their innovation because they now have something they have never had before: real-world operational data, genuine customer feedback from actual deployment conditions, and a technical baseline against which the next generation of the technology can be developed with precision.

Therefore, the FOAK is not the end of the technology development journey but the point at which technology development becomes genuinely interesting. The difference now is that operational reality is guiding their development, not inspiration or observation from the lab.

As we discussed earlier, companies can also find that by the time they turn their attention to the next generation of the technology, the gap between what they have deployed and what the market now expects has widened. Competitors who may not have the technical pedigree of the original innovator have been able to move faster precisely because they were not carrying the complexity of a live deployment. We have seen this happen to clients multiple times over the years.

How to respond?

The answer is not to underfund the FOAK delivery but to recognise, from the outset of TRL 8, that innovation continuity is itself a strategic requirement – and to move forward and build the organisational capacity required to sustain it. Some companies do this by maintaining a dedicated R&D function that is explicitly insulated from the delivery pressure of the FOAK. Others build it into the mandate of the technical leadership, with a clear expectation that next-generation development begins before the first-generation deployment is complete.

What matters is that the company does not arrive at TRL 9 with a single commercial deployment, a team that is exhausted from delivering it, and no clear line of sight to what comes next. The companies that do arrive in this condition rarely recover the momentum they need to compete at scale.

6. Capital, Credibility, and the Series B

By TRL 8, the capital requirements have grown to a scale that makes every previous funding conversation look modest.

The Series B is the round most commonly associated with funding the FOAK and the early stages of the Nth-of-a-kind buildout, and it is a qualitatively different kind of capital raise. Pre-seed and seed investors backed the founding team and the technology concept. Series A investors backed the evidence of operational viability from the pilot. Series B investors are being asked to fund actual commercial deployment at a scale that, in most Deep Tech sectors, represents a material financial commitment. The numbers are larger, the due diligence is more intensive, the investor profile is different, and the expectations of what the company needs to demonstrate are considerably more demanding, as we have seen.

What Series B investors are buying, fundamentally, is the conviction that the company can execute at commercial scale. It is not just about the technology working – that should have been established at TRL 6 and 7. It is not just about whether there is a market – that should have been evidenced by the commercial relationships developed through the Pilot Stage. What they need to believe is that the organisation, the leadership, the supply chain, and the commercial infrastructure are sufficiently mature to deploy capital effectively. In Phase IV language, they are asking: can this organisation scale without breaking itself?

This means that the Series B conversation begins long before the Series B round is opened. It begins with the quality of the Series A investor relationships and how those investors have been managed through the Pilot Stage. It continues with the credibility of the FOAK customer relationship – whether that customer is visibly committed, technically engaged, and willing to be a reference. And it is shaped, significantly, by the quality of the leadership team that has been assembled by the time the conversation happens.

Grant funding and government support remain important at this stage, particularly in capital-intensive Deep Tech sectors where public investment in critical technologies continues to be substantial. Such funding serves a different purpose than at TRL 5 and 6. It is less about technical validation, and more about reducing the risk-adjusted cost of capital for private investors, and extending the runway to allow the company to optimise the FOAK before the full Series B is deployed.

The companies that navigate TRL 8 most successfully are those that treat the capital strategy as a function of the delivery strategy, and not a separate workstream. The pace at which capital is raised should be calibrated to the pace at which the organisation can absorb and deploy it effectively. Raising too much too early, before the organisational infrastructure to use it well is in place, is one of the more common and costly mistakes of the FOAK stage – one that Series B investors, in retrospect, often acknowledge they should have spotted sooner.

7. In Closing

By the end of TRL 8, the company should be a different kind of entity from the one that entered it – different in how it is organised, how it makes decisions, how it develops and deploys its technology, how it raises and deploys capital, and how it thinks about the market in which it is operating.

Phase III will have been completed: the irreversible choices made, the constraints accepted, the commitment to a specific application and customer context demonstrated. And Phase IV will have begun in earnest: the governance designed, the systems built, the culture deliberately shaped for scale rather than simply preserved from the founding days.

The companies that achieve this are the ones that treated TRL 8 as what it actually is: the stage in which a start-up decides to become a serious company.

Deep Tech Leaders is building the ‘data-first’ operating manual and talent network for companies navigating the Lab-to-Market journey. Through domain-specific data & insight, long-form analysis, in-depth conversations, and our world-leading talent network, we surface how Deep Tech companies actually progress – and why so many fail. This work is underpinned by our executive search practice focused on placing proven leadership talent into roles where phase, risk, and capability align.